Accounting

SMB Optimism Stays Flat in August

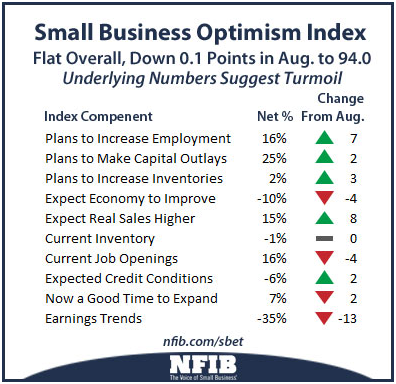

Small-business optimism remained flat in August, dropping 0.1 points from July for a final reading of 94.0, showed NFIB’s Small Business Economic Trends, a monthly survey of small business owners’ plans and opinions.

Sep. 10, 2013

Small-business optimism remained flat in August, dropping 0.1 points from July for a final reading of 94.0, showed NFIB’s Small Business Economic Trends, a monthly survey of small business owners’ plans and opinions. The report is based on the responses of 759 randomly sampled small businesses in NFIB’s membership, surveyed throughout the month of August.

While the total reading showed essentially no change over the month prior, a look at the individual indicators reveals incongruent details. Job creation plans leapt to a level not seen since before the recession and sales expectations improved; but this optimism would appear to contravene the dramatic deterioration in quarter to quarter sales and profit trends.

The favorable employment plans also contrasted sharply with the increasingly negative expectations for improved general business conditions. The month’s performance proved poor, but expectations, pre-Syria, were looking up.

“August in Washington was typical – nothing got done, and therefore nothing changed the outlook of small-business owners who have the same list of concerns today that they had in January, April and July,” said NFIB chief economist Bill Dunkelberg.

“But we saw some interesting things happening with the Index this month. The August reading provided us with a rather perplexing set of statistics; internally consistent on some dimensions, such as lower sales bringing lower profits, but contradictory in other ways, such as lower job openings but huge gains in hiring plans. We know that the upcoming implementation deadlines for the healthcare law are weighing on the minds of employers, and the current dim prospects for real tax reform must be, as well. The September survey will hopefully straighten things but with Syria on the horizon, the budget situation still up in the air, and Obamacare being rolled out, clarity over our economic direction is not likely to be the outcome.”

A review of the August indicators is as follows:

- Job Creation. August marked the fourth consecutive month of negative job growth for small-business owners. The average increase in employment for small firms surveyed was negative 0.3 workers per firm. Dramatic employment reductions have ceased but hiring has not resumed at normal levels.

- Hard to Fill Job Openings. Sixteen percent of all owners reported job openings they could not fill in the current period (down 4 points), and 9 percent reported using temporary workers, down 6 points from July. Most new jobs being created are likely to be in the part-time category.

- Sales. The net percent of all owners reporting higher nominal sales in the past three months compared to the prior three months plunged 17 points to a negative 24 percent – the second steepest monthly decline in survey history. The net percent of owners expecting higher real sales volumes surged 8 points, to 15 percent of all owners, a new high for this recovery period.

- Earnings and Wages. Earnings trends took a hit in August with the major softening in sales, falling 13 points to negative 35 percent. Five percent of owners reported reduced worker compensation and 21 percent reported raising compensation, yielding a seasonally adjusted net 15 percent reporting higher worker compensation (up 1 point). A net 12 percent plan to raise compensation in the coming months, up 1 point.

- Credit Markets. Credit continues to be a non-issue for small employers, 7 percent of whom say that all their credit needs were not met in August, up 2 points from July. Twenty-nine percent of owners surveyed reported all credit needs met, and 49 percent explicitly said they did not want a loan (64 percent including those who did not answer the question, presumably uninterested in borrowing).

- Capital Outlays. In August, the frequency of reported capital outlays over the past six months rose 3 points to 57 percent. The percent of owners planning capital outlays in the next three to six months rose 2 points to 25 percent.

- Good Time to Expand. In August, only 7 percent characterized the current period as a good time to expand (down 2 points). The net percent of owners expecting better business conditions in six months was a net negative 10 percent, 4 points worse than July’s reading.

- Inventories. The pace of inventory reduction continued in August, with a net negative 11 percent of all owners reporting growth in inventories, 1 point down from July. For all firms, a net negative 1 percent (up 1 point) reported stocks too low, unchanged from July. Plans to add to inventories were up 3 points to a net 2 percent, in line with an improvement in expectations for sales growth.

- Inflation. Seventeen (17) percent of the NFIB owners surveyed reported reducing their average selling prices in the past three months (up 3 points), and 18 percent reported price increases (up 1 point). The net percent of owners raising average selling prices was 2 percent, down 2 points. As for prospective price increases, 21 percent plan on raising average prices in the next few months (up 5 points), and 3 percent plan reductions (unchanged). A net 20 percent plan price hikes, up 5 points.